join the newsletter to Turn your paycheck into passive income

Stairstep Retirement

Pick your own golden years

A realistic path to free time before 65

Most retirement advice gives you two options: grind full‑time until your 60s, or try to sprint to early retirement with extreme frugality. Stairstep Retirement is a middle path. It lets you work hard early, dial back in your 30s and 40s, and still reach financial independence around traditional retirement age.

This is the retirement path I personally follow. It’s not right for everyone, but for many people who want to enjoy more of their youth and family years, it can be a realistic, achievable plan.

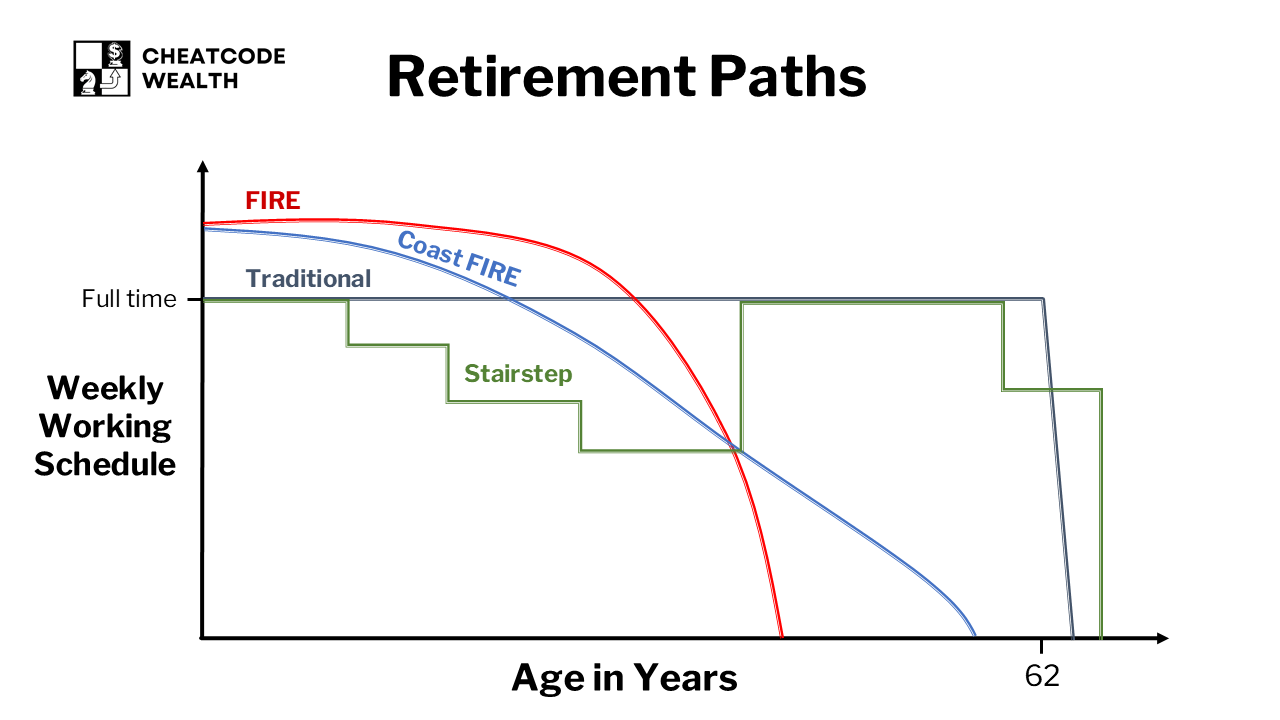

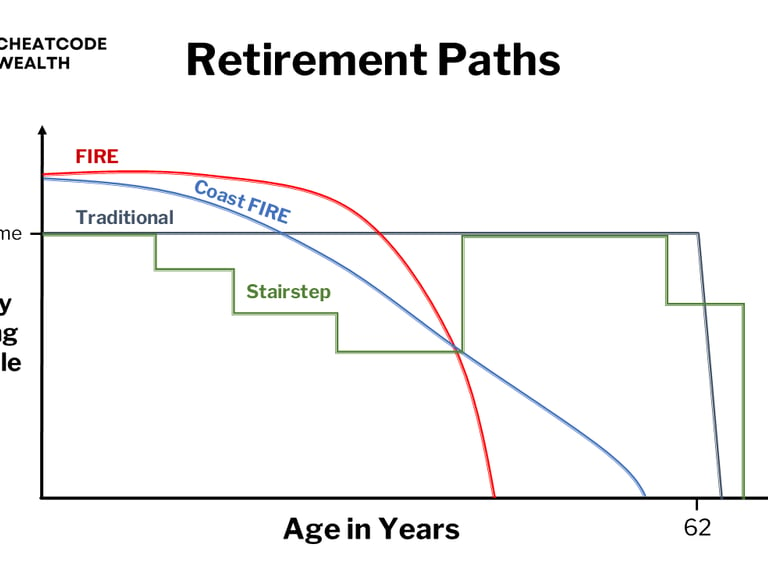

The Big Picture: Different Retirement Paths on One Chart

What you’ll learn on this page:

How Traditional retirement, FIRE, Coast FIRE, and Stairstep Retirement differ

Why Stairstep prioritizes free time in your 30s–40s instead of only in your 60s

Practical ways to reduce your work hours without quitting completely

How to decide if Stairstep Retirement might fit your goals and risk tolerance

On the chart above, you can see weekly work hours on the left and age along the bottom. Each line shows how many hours you work at different ages under a different retirement plan.

We’ll walk through each path, then zoom in on how Stairstep works.

Traditional Retirement

Traditional retirement is simple:

Work full‑time (often 40+ hours per week) from your 20s to your early 60s

Rely on salary, employer benefits, and slow, steady investing

Stop working completely around 62–67

On the chart, the Traditional line is almost flat at full‑time hours until it drops off near age 62. This is the default path for most people.

Upsides

Simple to understand

Fits most employer benefit structures

Low decision fatigue: you stay full‑time and save what you can

Downsides

Your best years of health and energy are spent mostly at work

Less flexibility for parents who want more time with kids

Retirement depends heavily on job stability and long‑term health

FIRE (Financial Independence, Retire Early)

FIRE tries to compress working life:

Work full‑time or more

Save and invest a very high percentage of income (often 50%+)

Aim to stop working completely in your 30s, 40s, or early 50s

On the chart, the FIRE line starts at full‑time but dives to zero hours well before your 60s.

Upsides

Maximum long‑term free time if it works

Forces high savings and intentional spending

Downsides

Can require extreme frugality or high income

Easy to burn out from the intense pace

Market risk: a long retirement window leaves more room for sequence‑of‑returns issues

May not be realistic for parents, caretakers, or people with lower incomes

Coast FIRE

Coast FIRE is a softer version:

Save and invest aggressively early on

Once investments are big enough to grow toward your retirement target without more contributions, you can “coast”

That often means switching to lower‑stress or lower‑pay work, or taking more time off

On the chart, Coast FIRE gradually slopes down from full‑time toward part‑time, hitting zero hours before traditional retirement age.

Upsides

More flexible than strict FIRE

Let's you take pressure off savings in mid‑life

Downsides

Still front‑loads the hardest work into your 20s and early 30s

Requires early investing discipline and at least some market comfort

If life happens (kids, health, layoffs), the “coast” phase may be delayed

Stairstep Retirement (the CheatCode Wealth Approach)

Stairstep Retirement takes pieces of all three:

The steady investing of Traditional

The focus on freedom of FIRE

The mid‑life flexibility of Coast FIRE

But instead of one big “on/off” switch, Stairstep uses intentional steps up and down in your work hours over time.

On the chart, the Stairstep line:

Starts at full‑time

Steps down in your 30s–40s

Steps back up later to top off savings

Eventually steps down again near traditional retirement age

You’re not trying to stop working forever at 35. You’re trying to re-balance work and life at each stage.

CheatCode Wealth™

Build your wealth. Keep your life.

© 2025. All rights reserved. Cheatcode Wealth LLC. This webpage may contain paid affiliate links.